The Collapse of Dubai’s Shopping Malls: From Global Icons to Ghost Towns

In 2024, Dubai Mall welcomed a record 111 million visitors and was widely celebrated as the beating heart of the city’s retail economy. Just two years later, in early 2026, the picture has changed dramatically. Foot traffic across many major malls has dropped by around 50%, while luxury sales in some locations have been cut in half. What was once presented as an unstoppable model of growth now appears increasingly fragile.

Here’s a closer look at five of Dubai’s most prominent shopping destinations and why they are struggling.

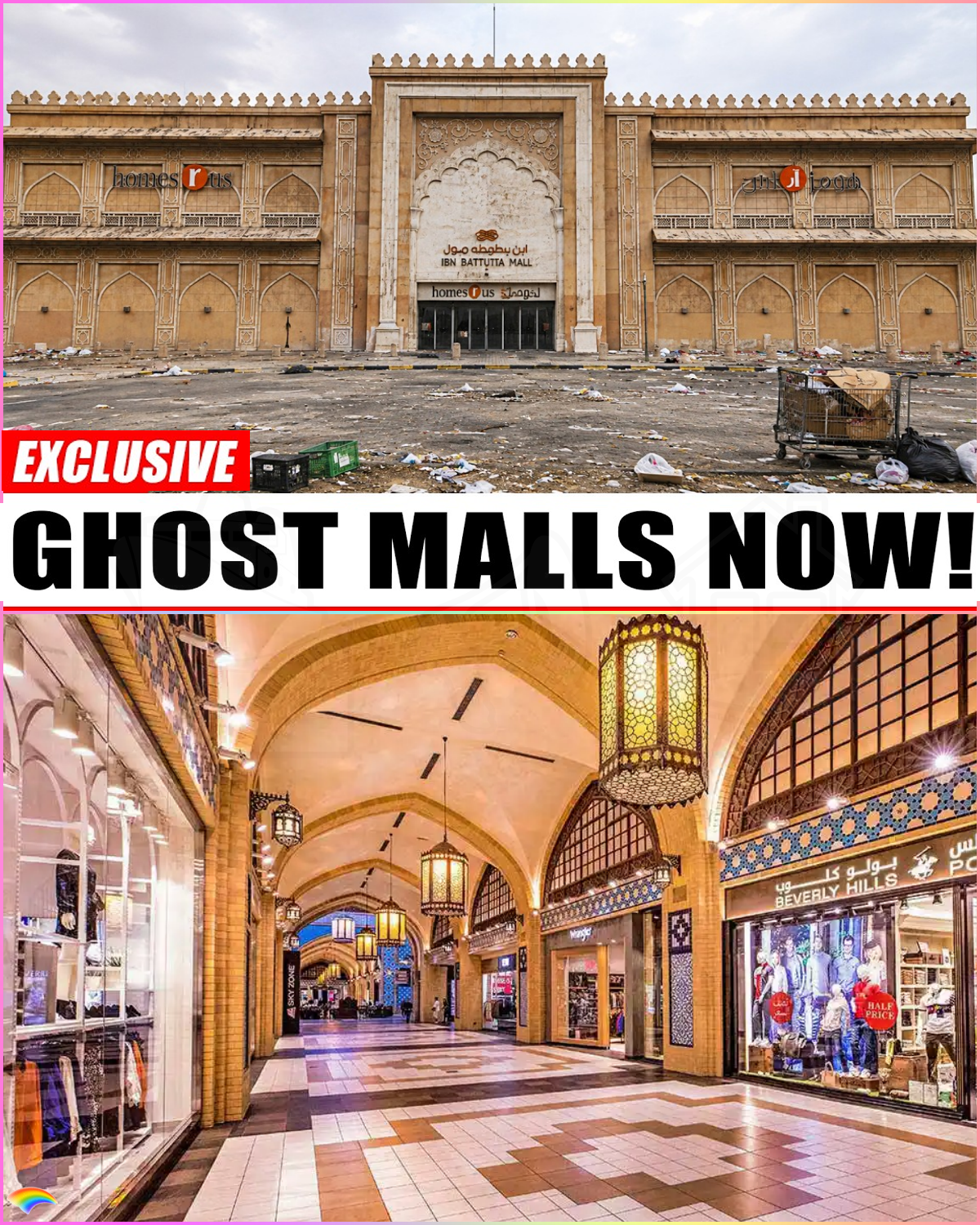

Ibn Battuta Mall: From Cultural Showcase to Public Utility

Once praised for its themed architecture representing different world cultures, Ibn Battuta Mall has seen a sharp decline. The departure of major anchor tenant Novo Cinemas removed a key reason for people to visit. With fewer visitors, many smaller stores have struggled, leading to rising vacancy rates.

The mall has attempted to reposition itself with more discount retailers, but this has created an awkward contrast with its original luxury and cultural theme. Today, many locals use it primarily as a place to escape the heat, visit the supermarket, or use the metro station rather than for serious shopping. The shift from a destination mall to a functional public space reflects how far its status has fallen.

Wafi Mall: The Worst Performer Among Major Malls

Wafi Mall has recorded the lowest performance among Dubai’s large shopping centers in recent rankings. High vacancy rates, particularly in the food and beverage sector, have created a noticeably quiet atmosphere. Many premium brands have chosen not to renew leases.

The mall’s older, more traditional architecture has also struggled to attract younger shoppers who prefer modern, experiential retail spaces. Attempts at renovation have been limited and have not reversed the decline. Long-time high-spending local customers appear to have moved on to newer developments or international shopping.

Dubai Mall: The Limits of Scale

Even Dubai Mall, long considered untouchable, has been affected. Luxury fashion sales reportedly dropped between 30% and 50% in the first quarter of 2026. Major brands including Louis Vuitton, Chanel, and Dior saw significant revenue declines, while Bloomingdale’s reportedly experienced drops of up to 60%.

The main drivers appear to be geopolitical tensions that reduced international flights and high-net-worth visitors from key markets such as Russia and China. While foot traffic remains relatively high, much of it now consists of casual visitors using the mall for air conditioning, photos, or the aquarium rather than spending in luxury stores. The gap between visitor numbers and actual sales has become increasingly obvious.

Nakheel Mall (Palm Jumeirah): Built for a Different Reality

Nakheel Mall was developed to serve the ultra-luxury residents of Palm Jumeirah. However, many of these residents now prefer shopping online through platforms that offer greater convenience and selection. The mall has struggled to attract consistent local spending.

A large portion of current visitors treat the mall as a transit point — stopping briefly on their way to The View at The Palm or the monorail rather than coming specifically to shop. With vacancy rates estimated between 35% and 40%, the center has failed to establish itself as a true destination despite its prime location and significant investment.

Dubai Festival City Mall: Over-Reliance on Airport Traffic

Located near Dubai International Airport, Festival City Mall once benefited from transit passengers and hotel guests. That advantage has turned into a major weakness. With flight cancellations and reduced international travel in early 2026, the mall has seen a sharp drop in its core customer base.

The riverside promenade and entertainment offerings have also suffered. Many visitors now watch shows or use the facilities without making significant purchases in the luxury stores. The mall appears increasingly dependent on IKEA and essential retail serving nearby residents rather than functioning as a high-end destination.

A Broader Pattern

These cases reveal several shared problems across Dubai’s retail sector:

- Over-reliance on international tourism: Many malls were built on the assumption of endless growth in visitor numbers. When geopolitics disrupted air travel, the model was exposed.

- Weak local spending: High-income residents increasingly shop online, reducing the need for physical luxury retail.

- Poor adaptation: Some malls have been slow to shift from pure retail toward mixed-use experiences that combine shopping, entertainment, and community spaces.

- Oversupply: Dubai built an enormous amount of retail space during the boom years. When demand softened, many centers were left competing for a smaller pool of customers.

What Comes Next?

Dubai’s malls were designed during a period of rapid expansion and almost unlimited ambition. The current challenges suggest that the old model — building ever-larger retail complexes primarily for tourists and assuming constant growth — is no longer sustainable on its own.

Some centers may successfully reinvent themselves as mixed-use destinations with stronger local appeal. Others may continue to struggle as their original purpose fades. What seems clear is that the era of treating massive shopping malls as automatic profit machines has come to an end.

The question now is whether Dubai’s retail sector can evolve beyond its dependence on volume tourism and create something more resilient — or whether more of these grand structures will gradually become expensive monuments to a different economic moment.

Disclaimer : This content may be created by AI for entertainment purposes. Any resemblance to real persons, events, or places is coincidental.